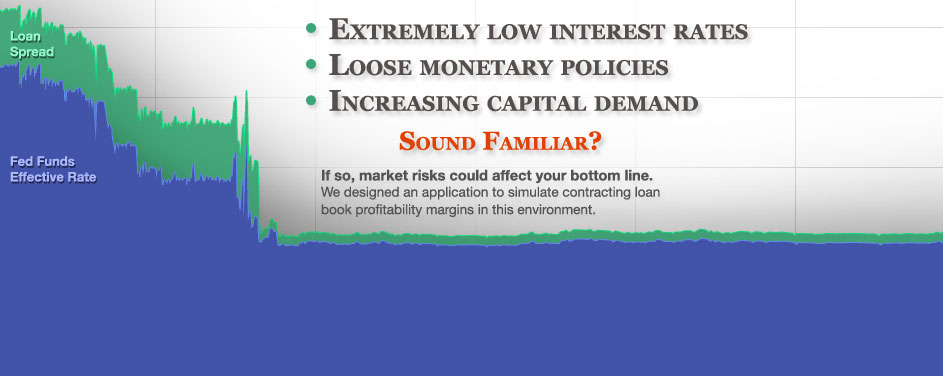

On April 6, 2016, the U.S. Department of Labor (DOL) issued its final rule expanding the “investment advice fiduciary” definition under the Employee Retirement Income Security Act of 1974 (ERISA) and modifying prohibited transaction exemptions for investment activities in light of that expanded definition. The new rule will go into effect on April 10, 2017, in a phased manner, with full implementation by January 1, 2018. The primary attributes of the new rule include:

- Significantly expanding the circumstances in which broker-dealers, investment advisers, insurance agents, plan consultants and other intermediaries are treated as fiduciaries to ERISA plans and individual retirement accounts (IRAs), and are therefore precluded from receiving compensation that varies with the investment choices made or from recommending proprietary investment products absent an exemption;

- Providing new exemptions, and modifying or revoking a number of existing exemptions, addressing those activities; and

- Retaining the ERISA distinction between non-fiduciary “investment education” and fiduciary “investment advice.”

Importantly, the DOL defines an “investment advice fiduciary” under this ruling as a service provider that acts in the best interests of clients, one who must enter into a Best Interests Contract (BIC) with clients who own or administer accounts governed under ERISA. Such investment advice fiduciaries can only receive compensation that is deemed “reasonable.” However, the DOL included A Best Interests Contract Exception (BICE), permitting these advice fiduciaries to receive commission-based compensation and compensation from 3rd parties, like mutual funds and insurance companies, if granted a prohibited transaction exemption (PTE).

Sounds like alphabet soup, doesn’t it? Net, eBISTM believes this ruling is a step in the right direction for retirement savers, but it does not go far enough. As a positive, it forces commission-based advice-givers to submit additional disclosure to investors about their sources of compensation and commit to a best interests standard with clients. The ruling does not, however, eliminate conflicts of interest, as brokers and advisers can still sell commission-based products to retirement clients that are either proprietary to their firm or include hidden marketing fees, which the DOL labels “conflicted compensation.” This situation introduces moral hazard if a high commission/proprietary/marketing-fee product is less appropriate for a client than a low commission/independent/no-marketing-fee product. Further, the DOL ruling does not require advisers to make investment recommendations in a financial planning context, which would require an understanding of the complete financial circumstances of the client.

eBIS holds itself to a much higher standard than the DOL mandates. eBIS has never accepted any type of commission or marketing incentive, a.k.a., conflicted compensation, and commits to the fiduciary standard in its purest form: always act in the best interests of clients, making recommendations as a prudent expert would while evaluating their specific financial circumstances. We feel a true fiduciary meets all of the following criteria:

- Bound by the “Prudent Expert Rule” in investment decision making.

- Employs Modern Portfolio Theory (MPT) in portfolio construction, focusing on investment risk, taxes, and costs.

- Requires a four year college degree, with a preference for advanced degrees, and industry-specific certifications to handle and manage client money.

- Fully discloses business practices, fees, and professional history in a readily available regulatory filing.

- Generates revenue through fees only, billed directly to the client, generated by either an hourly bill rate or an assets under management/advisement percentage. Does not accept performance fees.

- Avoids all conflicts of interest by rejecting referral/finder’s fees, affiliate fees, 12B-1 fees, revenue sharing, soft dollars, and any other direct or indirect compensation not emanating directly from the client.

- Engages any client through an account agreement, defining important details such as the structure of the advisory relationship, limited power of attorney (LPOA) rights and responsibilities, and remediation avenues in case of disputes.

- Compiles an investment strategy specific to the client after evaluating his/her full financial picture through a financial planning lens. Documents strategy in an Investment Policy Statement (IPS), from which the adviser cannot deviate without written amendments signed by both adviser and client.

- Defines a code of ethics against which all employees and contractors representing the firm are bound. Includes a pledge of integrity to act professionally and in the client’s best interests.

- Avoids self-dealing, including a trading policy that puts trades for clients’ accounts ahead of/in priority to employee trading.

- Never acts as a custodian of client assets. Engages an independent custodian, regulated by FINRA and insured by SIPC, at arm’s length from eBIS, to custody assets, process transactions, and report asset positions at least quarterly (with on-demand online access).

- Keeps client relationship and all client information confidential, bound by a non-disclosure and confidentiality agreement.

- Is regulated by an independent, state-specific regulatory authority or the Securities and Exchange Commission (SEC), not a self-regulating entity, e.g., FINRA.

We call this set of criteria the eBIS Fiduciary Standard, as we adhere to each of the points above, as delivered through our four fiduciary solution offerings: Retirement Plan Fiduciary Services; Financial Planning; Investment Management; Portfolio Risk Management. We believe all advisers providing investment advice should follow this highest standard. Being a fiduciary should mean nothing less.

About eBIS

eBIS is a Registered Investment Adviser, specializing in investment management, financial planning, and retirement plan fiduciary services. Since 2002, we’ve delivered solutions that help our clients implement sound investment portfolios, understand embedded risks, and improve risk-adjusted returns in a regulatory compliant manner. We strive to build bridges between strategic ideas and realized solutions by asking questions, generating consensus, and communicating in terms everyone can understand. We deliver solutions that are flexible, scalable, and adaptable as your situation changes. The company’s client list includes top ten international and U.S. financial institutions in commercial and retail banking, investment banking and asset management, as well as small and medium-sized businesses and individual investors. www.ebis.biz